Luxury Real Estate Trends in 2025

Collated from Different Sources: ET, FE, BS, FI

New home sales in India declined for the first time since the pandemic, as a sharp rise in housing prices and elevated borrowing costs ruined buyers’ appetite in 2024 and the real estate industry is now eyeing the upcoming Budget for favourable economic conditions — a key to reviving demand conditions. The de-growth in the Indian housing market came after three straight years of stellar growth, following the COVID-era downturn, and was attributed in part to a high base in the previous year, a fall in supply of new homes and price appreciation.

Anuj Puri, Chairman of Anarock, one of the leading housing brokerage firms in the country, termed the year 2024 as a “mixed bag” for the Indian residential market and noted that, while demand for the affordable housing segment was weak, sales and launches of luxury homes remained strong.

India’s residential real estate market, estimated to be valued at over USD 300 billion, faced a marginal 4 per cent drop in sales volumes during 2024, according to data from consultant Anarock. After a 47 per cent decline in 2020, housing sales had grown by 71 per cent, 54 per cent and 31 per cent in 2021, 2022 and 2023, respectively.

Post-pandemic, the ultra-rich started lapping up luxurious flats, villas and penthouses at launch itself and this year was no different.

“No doubt, the central and state elections played spoilsport to some extent, but it would also be fair to attribute at least some of the decline to the high base considering that in 2023 both new launches and sales had attained all-time high peaks,” Puri said.

Going forward, he expects the housing market to stabilize in 2025, with muted growth in prices, as against an average 21 per cent year-on-year rise this year. “Much also depends on what the upcoming Union Budget holds in store,” Puri said.

Real estate developers have a long-standing demand for an increase in the deduction limit of interest on home loans under the Income Tax Act to boost housing sales, particularly in affordable and mid-income categories.

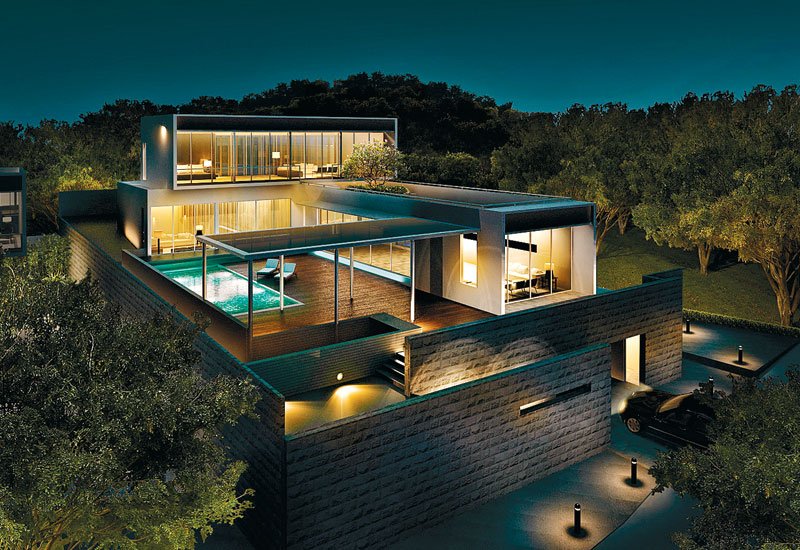

The luxury and ultra-luxury housing segment, which does not need any fiscal support, continued its upward journey.

Most of the real estate companies focused on luxury residential projects led by realty major DLF Ltd that launched a super luxury project ‘The Dahlias’ in Gurugram comprising around 400 units with an estimated sales value of Rs 26,000 crore — possibly the largest project announced so far in terms of revenue potential.

News of luxury residential projects getting sold within a few days of their launches became the new normal in 2024.

“2024 has been another monumental year for the Indian real estate sector, with residential demand still remaining robust on the back of heightened consumer interest and the shift towards buying instead of renting,” CREDAI National President Boman Irani told PTI.

The luxury segment has done particularly well, providing further validation of the evolving appetite of the Indian homebuyers who now seek better, bigger homes with enhanced lifestyles, he added.

In contrast to the housing segment, the office market saw record leasing of workspaces this year, with foreign companies looking to set up Global Capability Centres (GCCs) in India to capitalize on the availability of cheaper real estate and English-speaking skilled talent pool.

Gross leasing of office space across eight major cities is estimated to rise 14 per cent to touch a record 85 million square feet in 2023, according to Cushman & Wakefield data.

The demand for managed office space gained further momentum, prompting coworking operators to expand their portfolios in a big way.

To fund their expansion plan, coworking operators Awfis successfully launched its Initial Public Offering (IPO) this year, while Smartworks and IndiQube Spaces have filed preliminary papers with market regulator Sebi to launch their public issues.

The office market also got a filip from SEBI, which earlier this year approved regulation for Small and Medium Real Estate Investment Trusts (SM-RRITs) to boost investments in rent-yielding commercial properties. It is similar to REIT but as the name suggests smaller in scale.

Property Share Investment Trust launched India’s first SM-REIT public issue this year and there are many IPOs lined up for the next year in this space.

With a surge in e-commerce business and the government’s focus on boosting manufacturing activities in India, the demand for industrial and logistics spaces remained high this year.

Premium shopping malls continue to do good business helped by entertainment and food & beverages segments, encouraging builders to expand their retail real estate portfolio.

Being bullish on the long-term growth prospects of the sector, foreign and domestic investors infused huge capital in housing, office and industrial-logistics properties hoping for a better return on investment.

JLL India reported that Indian real estate attracted 51 per cent higher institutional investment in 2024 to nearly USD 9 billion, and experts believe that the trend will continue in the New Year on sustained demand across all asset classes.

Moreover, consolidation in the real estate sector gained further momentum this year, with consumer demand continuously shifting towards reputed players having better track records of executing projects.

To cater to this shift in demand, big and branded real estate players were very aggressive in land acquisition through outright purchases as well as entering into joint ventures with landowners.

There were also some positive developments this year on the old stalled housing projects front.

Mumbai-based realty firm Suraksha Group got a green signal from the National Company Appellate Tribunal (NCLAT) to acquire Jaypee Infratech Ltd through an insolvency process and complete around 20,000 units.

At the fag end of the year, the National Company Law Tribunal (NCLT) allowed state-owned NBCC to complete 16 real estate projects of Supertech Ltd. NBCC is already completing the stalled projects of erstwhile bankrupt Amrapali Group on the direction of the Supreme Court.

The successful resolution of these stuck projects holds the key to regaining consumer trust in India’s property market, even as homebuyers stuck in stalled projects of Unitech Ltd did not get any solution even this year.

In a nutshell, Indian real estate was more or less able to sustain demand in the housing segment, while achieving growth in office and warehousing verticals.

Real estate experts are confident about better performance of the housing segment next year, provided prices remain under control.

The sector can grow faster if the RBI cuts interest rates in its monetary policy and the Centre announces tax incentives for individuals and developers in the upcoming central Budget, industry players believe.

Irani of CREDAI feels that the real estate sector still faces “policy-related roadblocks that hinder its full potential”.

“Going into 2025, we are optimistic of government interventions to streamline certain policy roadblocks, especially for the affordable housing segment, to improve feasibility and address affordability concerns,” he said.

Irani stressed the need to redefine affordable housing, expand 80C benefits, and reduce interest rates to propel growth in Indian real estate, whose market size — as per Naredco-Knight Frank report — stood at nearly USD 500 billion in 2022 and is estimated to reach USD 5.8 trillion by 2047.

As the sector looks ahead to 2025, the focus remains on innovation, high-quality living spaces, and catering to the needs of both domestic and global buyers. From the rise of tier-2 cities as investment hotspots to the growing adoption of smart technologies and green practices, the future of Indian real estate looks poised for dynamic evolution.

Giving his views on this, Ankush Kaul, President-Sales, Marketing & CRM, Central Park, says, “In 2024, the high-end property market was defined by a shift toward sustainability and smart home technology, with eco-conscious developments and seamless tech integrations becoming key priorities. Integrated communities gained popularity, offering holistic living experiences, while demand for premium locations and strong infrastructure remained high. Privacy, security, and exclusivity also became essential, with buyers seeking advanced security systems and secluded spaces.”

Now 2025 promises to be a dynamic year for the high-end property market, with sustained demand for premium properties in well-established locations.

“Sustainability will remain a key focus, with buyers prioritizing green technologies and energy-efficient designs. The digital transformation of the sector will continue, enhancing property design, marketing, and purchasing decisions. We expect continued demand for hybrid properties and community townships, offering luxury experiential living, privacy, and security to discerning buyers. As the world becomes increasingly interconnected, non-resident buyers will remain a significant force in the luxury market, driving demand for properties with global appeal,” adds Kaul.

The Indian real estate sector continues to demonstrate resilience and adaptability, fueled by urbanization, government support, and the rise of sustainable, technology-driven projects. Tier-2 cities are rapidly gaining ground as they become more attractive for residential and commercial investments, driven by urban migration, affordable living, and government infrastructure initiatives.

“These cities offer substantial growth potential, with increased demand for quality housing and business spaces. The Manglam Group has been at the forefront of this shift, with successful project completions that contribute to the region’s development. By focusing on delivering high-quality residential and commercial properties in emerging markets, Manglam has aligned its growth with the demand for sustainable, future-ready spaces,” says Amrita Gupta, Director of the Manglam Group and Founder President of CREDAI Rajasthan Women’s Wing.

Looking ahead to 2025, the real estate sector will continue to evolve with a strong emphasis on meeting consumer needs. “The focus will be on launching projects that integrate innovation, sustainability, and advanced technology. As tier-2 cities continue to develop, they will be a key driver of India’s real estate growth, offering a wealth of opportunities for developers, investors, and residents alike,” she adds.

Mohit Goel, Managing Director of Omaxe Group, says, “The year 2024 has been a transformative one for Omaxe and the Indian real estate sector as a whole. Our successful launch of the landmark project in Dwarka marked a significant milestone, reinforcing our commitment to creating world-class infrastructure that caters to the evolving aspirations of homebuyers. This year, we witnessed unprecedented growth in the luxury housing segment, driven by a surge in demand from discerning customers seeking exclusivity, superior design, and value-driven investments.”

With 2025 on the horizon, the sector is set to achieve remarkable progress, supported by a projected 7% CAGR and an anticipated 10% increase in residential property sales. “This sustained momentum reflects the growing confidence in the Indian economy and the increasing value placed on high-quality living spaces. At Omaxe, we remain steadfast in our vision to redefine urban living through innovation, sustainability, and excellence. The coming year will see us further enhance our portfolio to meet the dynamic needs of modern India, contributing meaningfully to the nation’s real estate growth story,” adds Goel.

The Indian real estate sector demonstrated remarkable adaptability in 2024, driven by a surge in residential demand, increased NRI investments, and a notable expansion in the luxury housing segment.

“At Axis Ecorp, we take pride in pioneering the concept of fractional ownership, which is reshaping how investors approach premium holiday homes. This innovative model not only democratizes access to luxury properties but also optimizes rental yields, making high-end real estate a lucrative and attainable asset class. Goa remains central to this strategy, with its growing appeal among domestic and international buyers and consistently strong rental returns. As we step into 2025, the outlook remains highly optimistic. We foresee the continued popularity of fractional ownership alongside robust growth in the luxury segment, setting new benchmarks for investor interest and market performance,” says Aditya Kushwaha, CEO and Director, Axis Ecorp.

Here we take a look at what some other developers said about the performance of real estate in 2024 and the industry’s outlook for 2025:

Ramani Sastri, Chairman and MD, Sterling Developers: “The Indian real estate sector exhibited resilience and growth in 2024 bolstered by robust domestic demand, burgeoning aspirations and series of government driven infrastructure initiatives and is gearing up for a promising future. Home buyer confidence is at an all-time high and this naturally urges consumers to invest in their dream homes as the overall climate is geared towards sustained demand. While the residential real estate sector continues to show robust performance in the existing interest rate environment, we definitely hope to see lower interest rates next year which will provide further impetus to real estate and other sectors. The sustained demand will solidify the sector’s upward trajectory well into 2025, cementing the Indian real estate market as a key driver of economic growth.”

Manas Mehrotra, Founder, 315Work Avenue: “The co-working industry has become more relevant than ever with the demand surging significantly in the recent times owing to numerous factors. Co-working spaces have emerged as the defining feature of India’s rapidly evolving commercial real estate market, reflecting the broader shift toward work culture, flexibility, collaboration, innovation, and sustainability. The demand has gained greater traction with corporates and MNCs continuing to make a beeline to coworking spaces that have emerged as strong centres of growth. While major metro cities have been the key markets for co-working spaces, there’s a growing demand in tier-2 and tier-3 cities too, making the market more diverse. While co-working spaces continued to perform well in the recent past, we believe the share of coworking in the overall leasing of flex space is set to grow further and play a pivotal role in 2025 and beyond. As India’s workforce is becoming increasingly mobile, co-working spaces are well-positioned to cater to this dynamic shift with niche offerings. The demand for co-working spaces is expected to grow at around 20 per cent over the next two to three years.”

Vikas Aggarwal, COO, Worldwide Realty: “India’s real estate sector continues to demonstrate robust growth and resilience, supported by dynamic market forces and progressive government policies. Projected to achieve a trillion-dollar valuation by 2030, 2024 has already witnessed significant strides in affordability initiatives, commercial innovation, and sustainable practices. Landmark schemes like the Pradhan Mantri Awas Yojana (PMAY) have amplified housing accessibility, spurring growth in the residential segment and catering to diverse demographics. Simultaneously, the rise of flexible office spaces reflects the sector’s adaptability to hybrid work models and the growing demand for co-working setups. Looking ahead to 2025, the focus will shift to enhancing urban infrastructure and catalyzing growth in Tier 2 and 3 cities, unlocking fresh investment opportunities. With a dual emphasis on technology-driven solutions and sustainable construction practices, the sector is poised for steady and impactful progress, solidifying its status as a cornerstone of India’s economic growth.”

Vivek Sinha, Director-Sales & Marketing, KDMG Group: “2024 has been a transformative year for the real estate sector, with noteworthy progress in residential, commercial, and infrastructural developments. The adoption of sustainable practices, the growing integration of technology, and the emphasis on uber-luxury housing have reshaped consumer expectations. Key commercial hubs witnessed robust growth, driven by evolving business needs and hybrid work models. Infrastructure advancements, particularly in tier 2 and 3 cities, pave the way for long-term growth. The coming year is poised for a dynamic future, marked by innovation, digitization, and eco-conscious development, ensuring real estate continues to be a cornerstone of economic progress.”

NRIs to rule India’s luxury housing mkt

2025 is likely to witness healthy traction in luxury and ultra-luxury apartments and condos, driven by strong appetite from high net worth individuals( HNIs) and non-risident Indians (NRIs). A clear preference for premium and best-in-class offerings will increasingly define the contours of the segment. Enquiries and primary sales in plotted developments, villas within gated communities and vacation homes are likely to be strong throughout 2025 and beyond, said a report by Colliers India, a real estate consultancy firm.

Steady rise in average housing prices, which have increased 11 per cent in 2024, can have a stabilizing effect on the residential market in 2025, especially in the affordable housing segment, said the report.

Within residential real estate, demand for luxury and ultra-luxury segments will witness higher growth as compared to affordable and middle-income segments. Developers will continue to recalibrate their strategies and be selective in launching new projects. Amidst sustained housing demand, inventory levels, thus can drop further over the next few quarters. Ready-to-move-in properties and reputed developers with established project execution capabilities will continue to be preferred by homebuyers in 2025, it added.

Tier-II/III cities on an expansionary mode:

” With rapid urbanization and enabling factors such as infrastructure boost, tourism growth & employment opportunities, the organized residential market is likely to expand beyond the Tier-I cities, creating dispersed growth centers across the country. Real estate activity in the emerging smaller cities is on the rise, evident from established real estate developers foraying into these markets,” said Badal Yagnik, CEO of Colliers India.

Growing demand for senior living to create lucrative opportunities:

With India’s aging population projected to increase significantly by 2050, there will be a growing need for senior care and housing.

“Assuming the long-term potential in the sector, developers are likely to ramp up their activities in the senior living landscape during 2025. The senior living sector, currently valued at USD 2-3 billion, is poised for rapid growth, potentially reaching $10-12 billion by 2030. Although the demand-supply gap will continue to persist, market penetration and developer offerings are likely to pick up pace in both independent and assisted living formats over the next few years,” noted the report.

The year 2024 marked a pivotal moment for India’s luxury real estate market, as high and ultra-high-end properties emerged as the preferred choice for the country’s affluent as well as many real estate developers. Gurugram, Mumbai and Bengaluru remained the hey hotspots, while the trend towards premiumisation i.e. larger, more luxurious homes with better surroundings prompted developers to expand to traditional mid-end markets like Noida, Bengaluru, Pune, and Chennai.

Among the biggest individual deals in the year 2024, an upscale residential transaction in Delhi saw a bungalow of around 900 square yards sell for nearly ₹100 crore. In December 2024, 47-year-old Rishi Parti, the founder of Info-x Software Technology Pvt Ltd, bought an ultra-luxury 16,290 square feet penthouse at DLF Camellias, Gurugram’s Golf Course Road, also known as ‘North India’s Billionaires Row’, for ₹190 crore, thus bagging the crown of India’s most expensive purchase in 2024. Setting a new benchmark in India’s luxury real estate market, the transactions translated to a whopping ₹1.8 lakh per square foot for the carpet area and ₹1.2 lakh sq ft for the super area.

Notable 2024 purchases were recorded in Mumbai: Great White Global’s purchase of two apartments in Oberoi Three Sixty West, Worli, Mumbai, for ₹225 crore; a ₹198 crore 13,809-square-ft property deal by RR Kabel promoter Shreegopal Kabra; and a ₹263 crore three-flat deal in Lodha Malabar by Asha Mukul Agrawal of Param Capital.

The surge in premium and luxury housing demand prompted developers to launch numerous new projects, accounting for 19% of India’s total new residential launches in the January to September 2024 period, according to global property services firm CBRE’s year-end snapshot. Those investing in these high-end properties are also reaping huge returns. Estimates suggest the average prices of homes priced over ₹40 crore saw a 2% jump, while the average prices of homes in the more than ₹100 crore bracket surged 14% in the period.

The sale of ultra-luxury homes – units priced over ₹40 crore each – remained unabated in 2024 despite spiralling prices, according to real estate consultancy ANAROCK. A total of 25 ultra-luxury homes worth ₹ 2,443 crore (priced more than 40 crore) were sold till August 2024 alone, with cities like Mumbai, Hyderabad, NCR’s Gurugram and Bengaluru maintaining their positions as top choices for India’s rich. The 25 deals included 20 high-end apartments and five independent bungalows. Mumbai dominated with 21 ultra-luxury residential deals for around ₹2,200 crore — comprising 84% share of total deals. Of a total of 25 deals, at least 9 deals in 2024 were worth more than ₹100 crore each, all in Mumbai — 7 in South Central Mumbai & 2 in Bandra & Juhu.

While individual transactions saw record-breaking deals in 2024, broader trends in land deals and residential launches highlight an increasing appeal for luxury real estate in India.

Home prices up 23%, land deals up 65%

Amid escalating demand for luxury homes after the pandemic, there have been record new launches and sales of costlier homes across the top 7 cities. The average home price in India’s top 7 cities, including Bengaluru, Hyderabad, Chennai, Pune, Kolkata, NCR, and MMR, stood at ₹1.23 crore in H1 FY25 alone, an increase of 23% in a year. Anshuman Magazine, Chairman & CEO – India, South-East Asia, Middle East & Africa, CBRE, says a sustained momentum in residential land transactions and high-profile deals reflects strong investor confidence, favourable economic conditions, and India’s evolving real estate landscape.

“India’s land deal volume surged by 65% year-on-year till August, reaching around 1,700 acres. This growth was primarily driven by six major cities — Delhi-NCR, Mumbai, Chennai, Hyderabad, Bengaluru, and Pune. During this period, over 100 land transactions were recorded, marking a significant increase from the 60+ deals in the corresponding period of the previous year. “Delhi-NCR led the market with a 32% share of total land deal activity. Within the region, Gurgaon accounted for the largest share at ~65%, followed by Noida/Greater Noida at ~20%. Bengaluru, Mumbai, and Chennai followed with shares of 22%, 12%, and 10%, respectively. Collectively, these four cities accounted for ~75% of the total land deal volume.”

Rise in luxury housing and India’s wealthy

Demand for luxury and ultra-luxury homes has been scaling ever-rising heights since the pandemic, thanks to a spike in the number of India’s wealthy in the recent past. With demand soaring, developers have gone on a veritable launch spree for such high-priced homes. In 2022, 2023 and 2024 till August, over 99 ultra-luxury residential deals worth around ₹8,069 crore were closed in the top cities, as per ANAROCK data.

India ranks 6th globally in ultra-high net worth individuals (UHNI) population and third in Asia, trailing only China and Japan. The country’s UHNI count reached 13,600 in 2024, marking a 6% annual growth. This population is projected to soar by 50% by 2028, far outpacing the global growth average of 30%. India is home to over 850,000 high-net-worth individuals (HNIs), and this is projected to double to 1.65 million by 2027. Interestingly, 20% of these millionaires are under 40, signalling the growing influence of young wealth creators.

“India is witnessing a transformative era of wealth creation. From bustling metros to emerging Tier-II cities, the nation’s affluent population is expanding at a pace that is capturing global attention. A dynamic mix of young entrepreneurs, tech pioneers, and seasoned industrialists drives this change. The rise of high-net-worth individuals (HNIs, or people with investable assets of at least $1 million) and ultra-high-net-worth individuals (UHNIs, or those with assets worth above $30 million) in 2024 paints a fascinating picture of opportunity, influence, and ambition,” says Prashant Thakur, Regional Director & Head – Research, ANAROCK Group.

Outlook 2025

India’s real estate sector is poised to expand to $5.8 trillion by 2047, by when India aims to become a developed economy. If that happens, real estate’s contribution to GDP will expand to 15.5% from 7.3%. The premium and luxury housing segment will play a pivotal role in this expansion. In 2024, this segment saw its collective share of the overall residential demand increase from 6% in 2019 to 16% in the first nine months of 2024. “As luxury housing shifts gears from traditional bungalows to apartments and penthouses, we anticipate the premiumisation of amenities (in contrast to providing additional amenities) to be a key differentiator for luxury projects,” says Anshuman Magazine of CBRE.

With 2025 around the corner, demand for luxury and ultra-luxury segments within residential real estate will likely see higher growth compared to affordable and middle-income segments. “2025 is likely to witness healthy traction in luxury and ultra-luxury segments, driven by strong appetite from HNIs and NRIs. A clear preference for premium and best-in-class offerings will increasingly define the contours of the segment. Enquiries and primary sales in plotted developments, villas within gated communities and vacation homes are likely to be strong throughout 2025 and beyond,” says Badal Yagnik, CEO, real estate advisory firm Colliers India.

While it’s clear that India’s wealthy are driving the demand, one of the reasons behind increased prices across key cities, there are concerns that India’s middle class, which constitutes 31% of the Indian population, may be cutting back on spending in the wake of high inflation. Despite that, some of the stakeholders remain positive that 2025 will see a continued momentum towards premiumisation for long-term returns. “While the residential real estate sector continues to show robust performance in the existing interest rate environment, we hope to see lower interest rates next year, which will provide further impetus to real estate and other sectors. The sustained demand will solidify the sector’s upward trajectory well into 2025, cementing the Indian real estate market as a key driver of economic growth,” says Ramani Sastri, Chairman and MD of luxury property company Sterling Developers.